To achieve net zero emissions, industry - the biggest source of greenhouse gases - needs to rapidly scale up its use of carbon capture and storage (CCS) technology. CCS has been deemed a “necessity, not an option” by climate change experts for the UK to deliver net zero emissions. So far, the deployment of CCS has been slow and uneven, but there are signs of acceleration.

The Government may have softened its stance on certain green policies in recent weeks, but it remains “absolutely unequivocal” about sticking to its commitment to reach net zero carbon emissions by 2050. The U-turn on certain green targets (eg delaying the ban on sale of new petrol and diesel cars) doesn’t appear to have impacted the Government’s stated aim to capture and store 20-30 MtCO2 (including removals) per year by 2030 through the deployment of CCS/CCUS facilities in the UK.

To avoid compromising the UK’s overarching net zero plans, the Government has confirmed a raft of new carbon capture facilities designed to negate the emissions created by industry. G&T is playing a key role in delivering CCS/CCUS facilities that will form the start of the ‘East Coast Cluster’ – a project uniting the Humber and Teesside with an unparalleled and diverse mix of infrastructure to decarbonise industry. This article explores what carbon capture and storage is, how it works and why we need it. It also explores the UK’s current plans with regards to CCS/CCUS technologies, the role G&T is playing in helping to deliver these key facilities, and what the potential concerns are relating to their deployment.

What is carbon capture and storage?

CCS is a group of technologies that can capture carbon dioxide produced by major factories and power plants from industrial activity (ie steel or cement manufacturing). The aim is to prevent the carbon from reaching the atmosphere, thereby reducing carbon emissions and helping to tackle climate change.

Keeping the carbon from entering the atmosphere is done via a three-step process:

- Capturing the CO2

- Transporting the CO2

- Storing the CO2 underground (or reusing it)

Ironically, the technology was initially developed by oil and gas companies to produce more fossil fuels. Captured CO2 was pressurised and then pumped back into old oil wells to increase the pressure inside the reserve and dislodge any remaining hydrocarbon – a process known as ‘enhanced oil recovery’ or EOR. This is antithetical to how the technology is now being talked about by Governments, namely as a way to reduce carbon emissions.

How it works?

Capturing the CO2

In the first step of the process, CO2 is captured from large sources (ie power plants, natural gas processing facilities and even from the open atmosphere). There are three main methods to remove or ‘scrub’ the CO2 from power plants – post-combustion, pre-combustion and oxyfuel combustion.

- Post-combustion: separates CO2 from the flue gas, by using a chemical solvent for instance, after the fuel is burnt.

- Pre-combustion: involves converting the fuel into a gas mixture consisting of hydrogen and CO2 before it is burnt. Once the CO2 is separated, the remaining hydrogen-rich mixture can be used as fuel.

- Oxyfuel: involves burning a fuel with almost pure oxygen to produce CO2 and steam, with the released CO2 subsequently captured.

Post-combustion and oxyfuel technologies can be fitted to both new and existing plants but pre-combustion methods are less suited to existing plants given the larger modifications to the facilities involved. In addition to capturing the CO2 present in flue gas, it’s also possible to capture it directly from the atmosphere, using fans to draw in air and passing it through an environment consisting of solid sorbents or liquid solvents. However, this method is far more energy-intensive and less effective than capturing the CO2 from flue gas (which has a much higher concentration of carbon).

Once captured, the CO2 is compressed into a liquid state and transported.

Transporting the CO2

The captured CO2 can then be transported by pipeline, ship, rail or by road via tankers to a site for storage. The most common and efficient method, however, is by pipeline, using pressure to facilitate its flow to other locations.

To enable CCS on a large-scale, we will need more pipes and a greater carrying capacity of those pipelines. Although there is no precedent for CO2 pipelines in the UK, the formal planning application process is likely to be non-trivial, especially if the pipelines are routed underneath settlements.

Storing the CO2

The CO2 is then injected into geological formations, deep underground for permanent storage –typically in depleted oil and gas reservoirs, coalbeds, or deep saline aquifers. The carbon can even be pumped into non-depleted oilfields to force out any remaining pockets of oil (ie through the aforementioned EOR process).

Burying the CO2 underground – usually at a depth of 1km or more – prevents it from reaching the atmosphere and contributing to climate change. According to the Global CCS Institute[1], underground storage space isn’t the limiting factor that many assume. In fact, there is more underground storage resource than is actually needed to meet climate targets. Almost every high-emitting nation has already demonstrated having its own substantial storage resource.

One such storage site for the proposed Zero Carbon Humber project in the UK is called ‘endurance’ – a saline aquifer located in the southern North Sea, around 90km offshore. The site has the potential to store very large amounts of CO2.

Alternatives to Storage

As well as CCS, there is a related concept – CCUS (or carbon capture utilisation and storage) – which instead of storing the carbon, re-uses it in industrial processes.

Although most CO2 will be piped underground, the primary aim is to stop the CO2 escaping into the atmosphere and exacerbating the climate crisis. Therefore, an alternative to storage is to use the captured CO2 as an input for commercial products, such as manufacturing plastics, biofuel or carbonating fizzy drinks! These are industries where CO2 is considered crucial and where there isn’t currently an answer for replacing its usage. However, the potential implications of commercial use of captured CO2 on the climate are currently unclear. Although CO2 usage or utilisation provides a revenue source that makes the economics of carbon capture a lot more attractive, it does not necessarily reduce emissions or deliver a net climate benefit[2]

and so further research is required to assess its implications.[3]

Why do we need CCS/CCUS?

In short, CCS/CCUS is expected to play a key strategic role in meeting global climate change targets. Leading organisations and governments are all relying on a rapid expansion of CCS/CCUS to limit carbon emissions as part of their long-term energy outlooks.

CCS/CCUS technologies offer a promising solution for curbing emissions in industries notorious for their resistance to decarbonisation (or that are hard to decarbonise despite their efforts), such as steel, cement and chemicals. These sectors pose a challenge due to the substantial costs associated with transitioning them to cleaner energy sources. Moreover, these technologies play a pivotal role in generating low-carbon electricity and hydrogen (see here for more information), thereby enhancing the energy mix's diversity and facilitating the transition of a broader spectrum of sectors away from fossil fuels. Additionally, CCS/CCUS technologies contribute significantly to the extraction of existing CO2 from the atmosphere.

Increasingly compelling evidence suggests that the extraction of carbon dioxide from the air will play a crucial role in achieving a global state of net zero emissions. As underscored by the Intergovernmental Panel on Climate Change (IPCC), carbon dioxide removal through CCS/CCUS technologies is unavoidable if net zero emissions are to be achieved. Furthermore, CCUS projects have the potential to slash global carbon dioxide emissions by almost one-fifth and concurrently reduce the cost of tackling the climate crisis by 70%, as highlighted by the International Energy Agency (IEA).[4]

Nevertheless, CCS/CCUS ought to serve as a supplement to, rather than a substitution for, broader initiatives in carbon mitigation.

CCUS in the UK: Charting a Course

The Government sees potential for the UK to lead in CCUS technologies globally, becoming one of the greatest CO2 storage bases in Europe.

With a reputation as an international centre of engineering excellence, Grant Shapps, the previous Secretary of State for The Department for Energy Security and Net Zero (DESNZ), believes the UK can utilise its extensive experience in the oil and gas sector, as well substantial CO2 storage potential, to be a first mover in the CCUS space.[5]

The Government’s goal is to establish two CCUS ‘clusters’ by the mid-2020s and a further two by 2030, through which the Government aims to capture 20-30 MtCO2 per year. However, the UK is capable of supporting many more clusters. Theoretically, there is an estimated 78 billion tonnes of CO2 storage capacity in the UK continental shelf – i.e. the region of waters surrounding the United Kingdom, in which the country has mineral rights. This is one of the largest potential CO2 storage capacities in Europe.[6]

So where will these CCUS facilities be built? It invariably makes sense to build these new CCUS clusters near large sources of carbon emissions from industrial activity. Multiple emitters in these regions can then benefit from shared transportation and storage infrastructure, as the upfront cost of building this infrastructure is typically too expensive for just one emitter to cover themselves (compared to other abatement options) and would likely far exceed its needs.

In the Government’s cluster sequencing process map[7], clusters sequenced for the mid-2020s are called ‘Track-1’ clusters.

G&T is directly involved in delivering facilities that will form that start of the CCUS clusters in both Humberside and Teesside.

Net Zero Teesside

Net Zero Teesside will become the world’s first gas-fired power plant with carbon capture and storage facilities, producing up to 860 megawatts of electricity, enough to power around 1.3 million homes. Up to two million tonnes of CO2 emissions from the power station will be captured per year and transported offshore for storage.

It is estimated this multi-billion-pound mega project will create up to 5,500 jobs during construction with the plant coming online in 2028.

G&T is providing specialist cost estimating services to our client for the Net Zero project, as well as providing insights into the tier 2 market which is critical to successfully delivering a project of this scale.

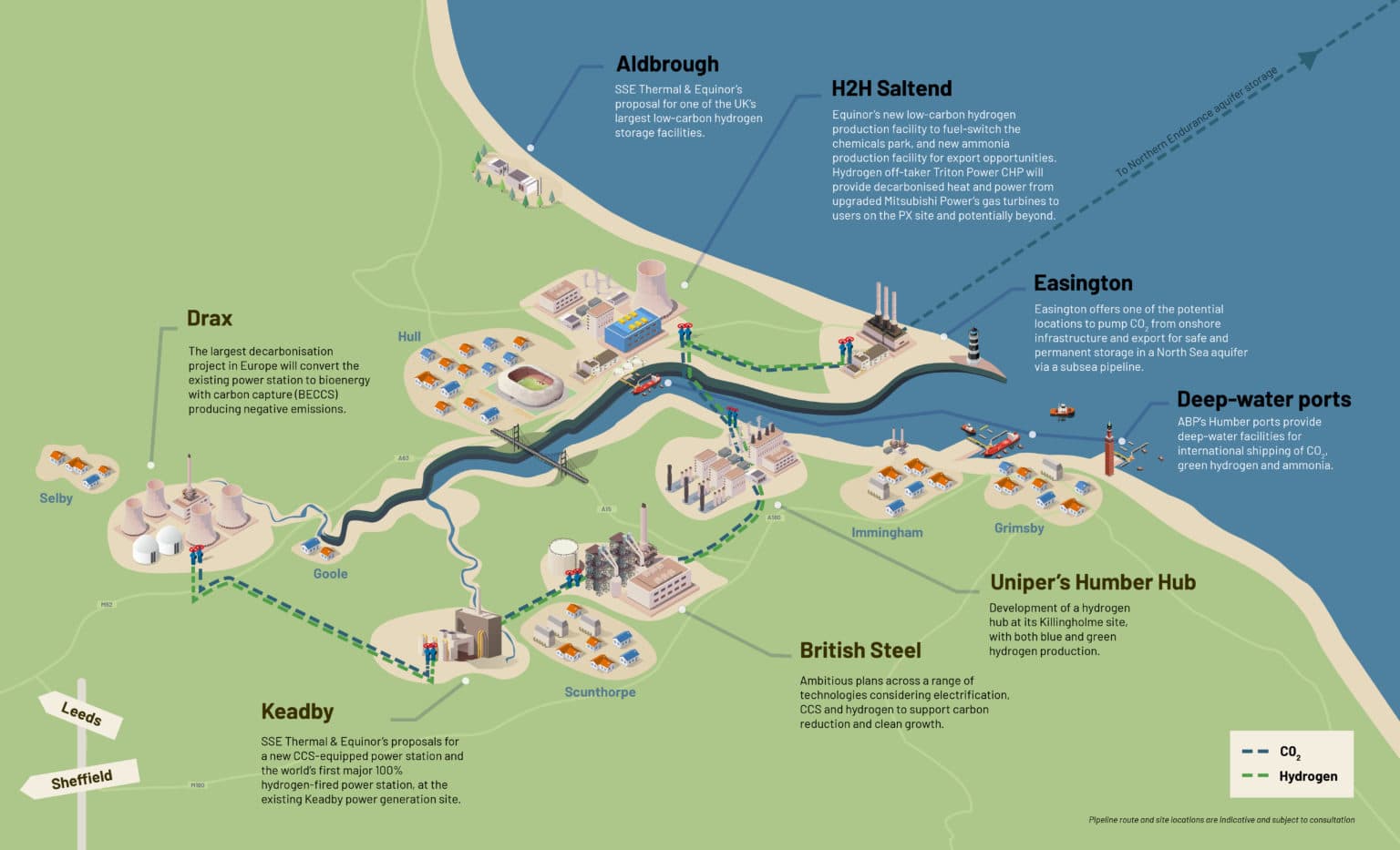

Zero Carbon Humber (Keadby 3 Carbon capture):

Supporting the ambitions of the ‘East Coast Cluster’ – a collaboration between Zero Carbon Humber, Net Zero Teesside, and Northern Endurance Partnership – Zero Carbon Humber aims to build the world’s first net zero industrial region.

The Humber is the most carbon intensive industrial cluster in the country. Developing carbon capture usage and storage (CCS or CCUS) and low carbon hydrogen technology in the region will be necessary to meet the UK’s emission targets.

Proposals for the region include low carbon hydrogen production, CCUS and shared onshore and offshore infrastructure. As part of these proposals, SSE Thermal and Equinor are actively developing Keadby 3, which could become the UK’s first flexible power station equipped with carbon capture technology by the mid-2020s.

Keadby 3 will connect to the shared infrastructure being developed by the East Coast Cluster to transport the captured CO2 and store it safely offshore.

With an electrical output of up to 910MW, Keadby 3 Carbon Capture Power Station will use natural gas as its fuel and will be fitted with a carbon capture plant to remove the CO2 from its emissions. Keadby 3 is expected to offset at least 1.5MT of CO2 from the atmosphere annually – 5% of the UK total.

G&T is providing specialist cost estimating services to our client for the Keadby 3 Carbon Capture project, as well as providing insights into the tier 2 market which is critical to successfully deliver a project of this scale.

What about isolated or inland carbon emitters?

The UK’s CCUS policy thus far has focused on establishing shoreline clusters. Although welcome, concerns have been raised that most emissions from hard-to-decarbonise industries (like cement production) originate from facilities located outside these proposed clusters. Currently, there is no formal strategy in place to tackle carbon using CCUS on dispersed sites.

According to a BEIS research paper[8], there are around 36 key dispersed industrial sites in the UK that would potentially be suitable for CCS. Together they emit an estimated 20.7MtCO2, with 87% of these emissions coming from iron % steel, cement, and refining. However, there are a number of risks and constraints associated with deploying CCS at these sites, making some sites more cost-effective than others. Although the study found that the dispersed location of a site can be a significant challenge towards CCS deployment (particularly at truly isolated sites with fewer emitters), it is not necessarily a showstopper.

What are the key concerns around CCS/CCUS?

Although carbon capture technology is often held up as a beacon of hope in reducing CO2 emissions, CCS at scale still faces short-term deployment challenges, usually relating to their feasibility, effectiveness and expense.

Even though CCS/CCUS technologies have existed for a few decades now, they are unproven at scale. Therefore, there some concerns about how these sites will work. However, it is the high cost of CCS/CCUS facilities that is perhaps one of the primary challenges.

High Costs

The current inflationary landscape has only added to concerns about the capital-intensive nature of building new CCS/CCUS facilities. The development, construction and operation of CCS facilities demand significant investments. The specialist equipment and infrastructure to capture the CO2, as well as the expenses associated with transportation and underground storage add to the overall cost.

Retrofitting operational facilities with carbon capture technologies can also be a complex and expensive endeavour. This is because each project is unique in terms of its design, size and installed equipment types. This can complicate the installation or modification of capturing technologies, thereby leading to cost escalations.

In addition to these high costs, the financial incentives of CCS/CCUS technologies to industrial operators are currently limited. Carbon capture is therefore seen by some as a pure cost. In the absence of a fixed, long-term carbon price, or even a global carbon tax acting as incentives, there are very few economic justifications for smaller, individual operators to adopt the technology. However, clustering, in which several facilities share CCS infrastructure and knowledge, can make CCS more cost efficient and economically feasible.[9]

Additionally, as the market expands and technologies develop, the cost of carbon capture technologies will inevitably fall.[10]

Other Challenges

Other challenges relating to CCS/CCUS that must be addressed for its successful implementation include:

- Finding and securing the right experts/partners across the supply chain.

- Labour shortages could make delivering CCS/CCUS projects difficult. Given the potential size of the proposed CCS cluster projects, resourcing will have to be carefully planned.

- Risks and uncertainties around the technological performance of CCUS operations.

- While there are vast underground reservoirs available, not all are suitable for long-term storage. Concerns about potential leaks or geological instability in some regions make site selection a complex and contentious issue.

- Social licence and public acceptance issues around the transport and store carbon (ie a ‘Not in My Backyard’ attitude), although this is less of an issue for offshore storage.

- Small risk that carbon may leak during transportation or from storage sites, leading to environmental damages and the reversal of CO2 emissions savings.[11]

- Some unresolved liability issues about who will insure/reinsure CCS projects against the risk of leakage from storage sites.

- Related to liability is the issue of who is responsible for the long-term monitoring of CO2 stored underground and addressing potential leaks (ie ensuring the integrity of the storage sites).

G&T is well-equipped to address several of these challenges and mitigate risk factors. With a proven track record of supporting the Department for Energy Security and Net Zero in various capacities, G&T brings extensive expertise to the table when it comes to managing major projects and engaging with supply chains. We aim to ensure the correct supply chain partners are selected, thereby minimising our clients’ exposure to commercial risk. Furthermore, G&T excels in providing comprehensive market analysis and facilitating early engagement with the supply chain. In today's dynamic market landscape, this proactive approach is crucial for the successful execution of major capital programs.

Ultimately, with climate targets becoming more ambitious, reducing CO2 emissions isn’t optional. Of course, the issues and concerns related to cost and risk need to be weighed against alternative decarbonisation methodologies, but many of the alternative pathways are either more expensive or less developed than CCS/CCUS. A recent article from the London School of Economics gave the example of steel production. It explained that incorporating CO2 capture into steel production raised estimated costs by less than 10%, but approaches based on hydrogen produced from renewables raised costs by 35–70% compared with conventional production methods.[12]

Finally, the cost of utilising needs to be considered against broader economic implications. Importantly, CCS/CCUS has the potential to enable energy-intensive industries to operate in a manner compliant with net-zero emissions goals, thereby safeguarding jobs and assets associated with these industries from becoming stranded.

Conclusion

Carbon capture and storage holds tremendous potential for reducing greenhouse gas emissions and mitigating climate change. The first priority should be the reduction of carbon emissions in the atmosphere, but as the only deep decarbonisation option currently available in some industries (ie steel or cement production[13]), the evidence suggests the UK would have little chance of reaching net zero by 2050 without employing CCS/CCUS. Where realistic decarbonisation alternatives do not exist, carbon capture technologies should be scaled up rapidly.

A strong domestic CCUS industry can create valuable economic opportunities for the UK by tapping into a growing export market. Therefore, the Government’s decision to support two new CCUS clusters is a positive step. However, the technology faces several challenges and concerns, including high costs, energy consumption, storage limitations, regulatory frameworks, public perception and long-term monitoring. The potential for stored CO2 to unintentionally leak is perhaps one of the biggest concerns. However, for well-selected, well-designed and well-managed geological storage sites, the IPCC says that risks are low – especially when the sites are positioned away from (natural and human-induced) seismic activity. However, addressing issues such as these is crucial to realising the full potential of CCS in the global effort to combat climate change.

The upshot is that CCS/CCUS is seen by scientists as a tool within a larger toolbox that can be used to reach our climate goals under the Paris Agreement. The other tools being blue and green hydrogen, electrification, wind and solar. However, CCS/CCUS shouldn’t be used to avoid deploying these other green tools; they all need to be deployed in parallel. This is the way to decarbonise our society.

[1] https://www.globalccsinstitute.com/wp-content/uploads/2018/12/Global-CCS-Institute-Fact-Sheet_Geological-Storage-of-CO2.pdf

[2] Once indirect and other effects have been accounted for.

[3] It is crucial to assess the climate impact of CO2 usage on a lifecycle basis, considering both the source and the end use of the CO2.

[4] https://www.iea.org/reports/transforming-industry-through-ccus

[5] https://www.gov.uk/government/publications/carbon-capture-usage-and-storage-net-zero-investment-roadmap/ccus-net-zero-investment-roadmap-capturing-carbon-and-a-global-opportunity

[6] https://www.gov.uk/government/publications/carbon-capture-usage-and-storage-net-zero-investment-roadmap/ccus-net-zero-investment-roadmap-capturing-carbon-and-a-global-opportunity

[7] https://www.gov.uk/government/publications/carbon-capture-usage-and-storage-net-zero-investment-roadmap/ccus-net-zero-investment-roadmap-capturing-carbon-and-a-global-opportunity

[8] https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/929282/BEIS_-_CCUS_at_dispersed_sites_-_Report__1_.pdf

[9] https://realiseccus.eu/ccus-and-refineries/industrial-clusters

[10] The cost of CCUS will continue to fall as the market expands and technologies develop. For example, the cost of CO2 capture in power generation reduced by 35% from the first to the second large-scale CCUS facility in that sector.

[11] However, this can be managed through regulation of project selection, management, and monitoring of storage sites. Many of the potential storage sites being considered are well-understood geological formations that have already stored gas and CO₂ naturally for millions of years, implying that leakage risk overall is relatively small.

[12] https://www.lse.ac.uk/granthaminstitute/explainers/what-is-carbon-capture-and-storage-and-what-role-can-it-play-in-tackling-climate-change/#:~:text=What%20are%20the%20key%20concerns,when%20energy%20costs%20are%20high

[13] Where the majority of emissions result from the process of chemical transformation as opposed to burning of fossil fuels